Visa has expanded the reach of its real-time push payments platform beyond cards with the launch of Visa Direct Payouts. As new partners join the platform, Visa is achieving its ambition of building a network of networks for real-time global payments providing cross-border connections for cards, bank accounts, and wallets. Robin Arnfield talks to Bill Sheley, Visa Direct’s SVP and global head

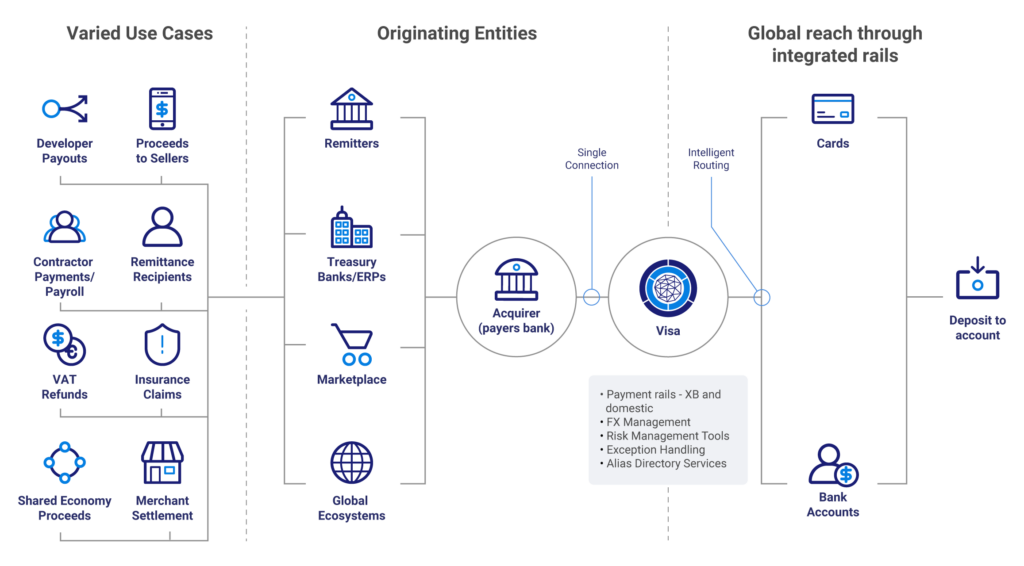

Visa Direct Payouts enables Visa’s clients and partners such as FIs, fintechs, remittance providers and corporate banks to use a single API-based point of connection to VisaNet. They can then push payments to eligible cards for domestic payouts, and to accounts and eligible cards for cross-border payments.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

“Prior to platforms such as Visa Direct, businesses wanting to provide cross-border transfers had to patch different solutions together,” says Sheley. “This is a complex and expensive process compared to the simplicity of integrating with Visa Direct. We are positioning Visa Direct Payouts as a platform for our global clients who want to originate payments to SMBs and consumers.”

The launch of Visa Direct Payouts follows the full integration of VisaNet and Earthport, which Visa acquired in May 2019. UK-based Earthport provides connections to banks, real-time payment (RTP) systems, and ACH networks around the world.

“We see ourselves as operating a network of networks for global connectivity,” said Sheley. “Users can fund Visa Direct transfers through cards, bank accounts or wallets, and we use intelligent routing to get the money to recipients’ cards, accounts and wallets. We connect to local payment schemes such as ACH networks and RTP systems through Earthport.”

“Visa Direct is multi-endpoint, multi-form factor, and multi-rail, connecting to over 3 billion cards and 2 billion bank accounts globally,” says Sheley. “Our system is set up to connect to any store of value, for example a prepaid card that sits under a wallet.”

Visa Direct supports alias directories, enabling users to link their bank account, wallet or card credentials to email addresses or cellphone numbers, so senders don’t need to know recipients’ financial details.

Visa currently clears transactions for Visa Direct over 65 domestic ACH networks, 16 card networks, five payment gateways, and 7 RTP systems. In Visa’s financial year ending 30 September 2020, Visa Direct processed nearly 3.5 billion global transactions.

In North America, Visa offers the Visa Push Payment Gateway Service to enable push-to-card capabilities for non-Visa cards. In other countries, Visa leverages its payment facilitator partners such as Adyen, Stripe, and Worldpay to act as the switch between Visa cards and non-Visa cards.

Use cases

Visa Direct currently has over 50 use cases, including P2P transfers, cross-border remittances, disbursements such as insurance claims and marketplace seller payouts, business-to-small business (B2SB) payments, payments to gig economy workers, and earned wage access.

Ensuring early access to salaries, earned wage access means that workers receive a percentage of their pay on demand, instead of waiting for their usual fortnightly or monthly salary cycle.

“We’ve been doing a lot of work in payroll via Visa Direct since 2019,” said Sheley. In the US, Visa is working with ADP and with earned wage access providers such as DailyPay, FlexWage, Instant Financial, PayActiv, and ZayZoon to provide fast payments to hourly-paid workers via Visa Direct. Visa has also formed a partnership with European early wage access provider Wagestream.

“Because of Covid-19, the earned wage access economy has become very big in the US, and we’re also seeing it in the UK and other countries,” said Sheley. “Employers now see earned wage access as table-stakes in order to attract and retain employees.”

P2P payment and cross-border remittance providers which Visa partners with for Visa Direct include PayPal and its Venmo and Xoom subsidiaries; Canadian processor Moneris, which is owned by RBC and BMO Bank of Montreal; US bank-operated P2P service Zelle; Facebook; Square; Google; MoneyGram and Wise (formerly TransferWise).

Domestic P2P Visa Direct transfers range between $100 and $150 and cross-border transfers range from $350 to $500, while insurance payouts range from $1,500 to $2,000, according to Sheley. Visa Direct transaction amounts are typically under $50,000.

In Peru, Visa Direct is used by five bank-operated P2P transfer services including Banco de Crédito del Perú’s Yape, which has over 5 million users; and PLIN, operated by Scotiabank Peru, BBVA and Interbank, which has 3 million users.

Sheley said the five Peruvian bank-provided P2P transfer services have seen massive growth. These services use alias directory technology from Latin American mobile payments firm YellowPepper, which Visa acquired in November 2020. YellowPepper’s platform enables consumers to use email addresses and cellphone numbers as aliases for their bank account numbers in P2P, B2C and G2P (government-to-person) transfers.

Visa Direct posts strong growth

Although the global cross-border remittance industry saw an estimated 7% decline in volumes in 2020 due to COVID-19, according to the World Bank, Visa Direct has continued to grow.

“Depending on the use case, we’ve seen 70-100% growth year-on-year in transaction volumes, although we saw a bit of a dip in March 2020,” said Sheley. “Insurance payouts remained quite resilient during 2020, and P2P transfers continued to grow quite heavily during the pandemic, especially after governments started to make stimulus payments.”

In the year to 30 September 2020, Visa Direct provided faster payouts to over 2.35 million US small businesses and sellers, according to Visa.

Visa Direct has seen growth in countries such as Guatemala and the Dominican Republic where governments use the platform because of its immediacy to make COVID-19 stimulus payouts, said Sheley. In Latin America, with its high percentage of unbanked and underbanked people, governments have been increasingly depositing social benefit payments to wallets, leading to a significant growth in wallet adoption in the region.

The gig economy is another growth area for Visa Direct. “During the pandemic, people were having their meals delivered to their homes instead of going to restaurants, so the use of Visa Direct to pay gig economy delivery drivers went through the roof,” said Sheley.

New services

Visa clients launching new services powered by Visa Direct Payouts include Standard Chartered Bank (Hong Kong), which is enhancing digital international transfer services for its retail banking clients, and MoneyGram which is rolling out an enhanced money-movement feature for its customers making cross-border remittances.

In 2019, MoneyGram became the first remittance provider to enable cross-border transfers from the US through Visa Direct. In Q4 2020, MoneyGram saw a 650% year-on-year transaction growth for Visa Direct.

In January 2021, MoneyGram partnered with UK-based processor Checkout.com to expand its real-time digital P2P payments service with Visa Direct. As a result, MoneyGram customers can transfer funds in real-time using its website or mobile app to Visa debit cardholders across 575 corridors from 25 European countries.

“Moneygram and other remittance platforms are trying to provide a much more digital experience,” says Sheley. “Operating a network of bricks-and-mortar cash-in and cash-out agents and ensuring they remain compliant is expensive. Replacing cash-based remittances with real-time cross-border authorised transactions provides a great customer experience and much easier transaction reconciliation and monitoring.”

KyckGlobal, a Visa fintech partner, is using Visa Direct Payouts to enable several B2SB and B2C use cases including insurance claims payouts, fast funds settlement for SMB marketplaces, and quick access to earned wages for independent contractors and hourly workers.