Cash remains the predominant payment instrument in Indonesia – especially among the rural population – accounting for 98.4% of the total volume of payments in 2017. This was primarily due to low awareness of electronic payments, a high unbanked population, and limited access to banking infrastructure. The modernisation of the country’s payments infrastructure with the introduction of the National Payments Plan, the transformation of cards to incorporate EMV technology, and the National Non-Cash Movement will support the transition to non-cash payments.

The government along with the central bank is aiming to further develop the electronic payment system in the country, with initiatives such as support for the development of a national shared ATM network and allowing foreign investments in the e-commerce sector. As the government and banks have taken various such initiatives, payment cards will grow steadily over the next few years and will gradually become more accepted.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

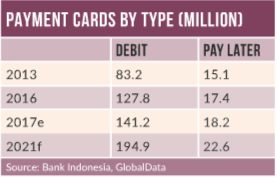

Debit cards maintain their stranglehold

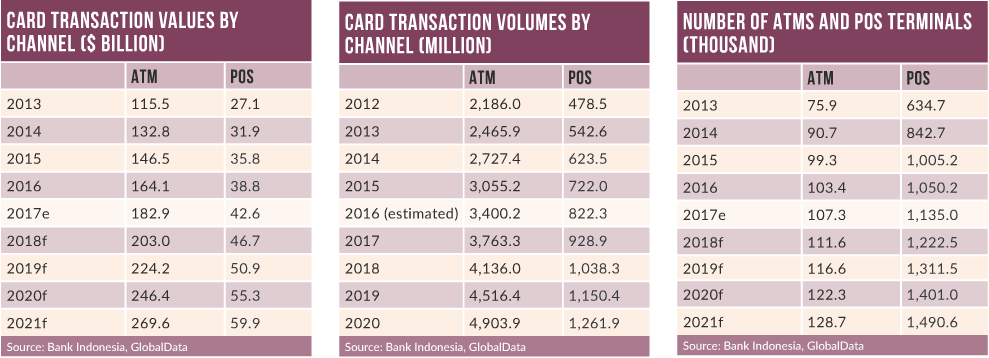

Debit cards remain the preferred payment cards among Indonesian consumers. However, usage is mostly restricted to ATM cash withdrawals, with frequency of use at 9 times that of POS transactions. This is primarily because both consumers and merchants still prefer the use of cash. However, with ongoing efforts by the government to enhance the POS infrastructure and card acceptance, the number of POS transactions has increased.

While the frequency of use of debit cards is anticipated to increase consistently over the period to 2021, the average transaction value at the POS will decline at a forecast-period CAGR of 0.7%. This shows the gradual migration of use of debit cards for low-value transactions at the POS.

However, there is still a long way to go for cards to reach truly regular usage levels, with the average card expected to be used only once every three months by 2021.

Stricter regulation led to low credit card adoption

Strict government regulation with regard to credit card eligibility remains one of the major reasons for the low penetration. Mounting card debt among consumers forced the central bank to introduce a regulation, effective since January 2015, according to which individuals with an annual income of less than IDR3m ($222) are prohibited from possessing credit cards.

Growing e-commerce to support payment growth

Growing e-commerce to support payment growth

Up until February 2016, the e-commerce market was in the government’s “Negative Investment” list – and thereby foreign investors were not allowed to invest in local companies or set up a business. To boost investment in the domestic e-commerce market, the government introduced a new foreign direct investment policy in February 2016 allowing 100% foreign ownership of e-commerce companies for investments over $7.4m, while for investments between $740,000 and $7.4m, foreign ownership was capped at 49%. However, the former regulation was later revised in May 2016 to limit foreign ownership to 49% in e-commerce companies.

The Indonesian e-commerce market rose from $1.9bn in 2013 to $10.7bn in 2017, supported by a growing young population, and the increasing presence of online retailers. The market is forecast to register a CAGR of 23%, which is the third highest compared to its peers – Pakistan (33%), India (24%), Vietnam (22%), the Philippines (21%), Thailand (17%), Malaysia (15%), and China (11%). This suggests there is significant growth potential in the Indonesian e-commerce market.