The payment card market in Belgium is well developed, with penetration of two cards per inhabitant.

Improved payment infrastructure, a strong banked population, a gradual shift from cash to card-based transactions, and the expansions of the retail and e-commerce markets have supported this growth.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Belgian consumers are very comfortable with established payment instruments, with domestic payment method Bancontact the most commonly used card scheme. The EU regulation capping interchange fees for banks operating in the EU, and a cap on cash transactions by Belgium’s central bank have also helped drive electronic payments.

With the increased adoption of mobile POS solutions by smaller merchants, electronic payments are set to surge over the next five years.

The launch of a contactless payment feature by Bancontact and the presence of Google Pay in Belgium are expected to provide a boost to the nascent contactless payment space.

Bancontact dominates

Belgian consumers strongly favour debit cards over other cards, and national scheme Bancontact is the most frequently used card. Until the EU cap in 2015, its low interchange fees compared to international schemes gave it a significant edge in the market – and the new fees have had little impact on its dominance.

Bancontact cards are now equipped with contactless functionality, enabling debit card holders to make transactions of up to €25 ($30) without entering a PIN.

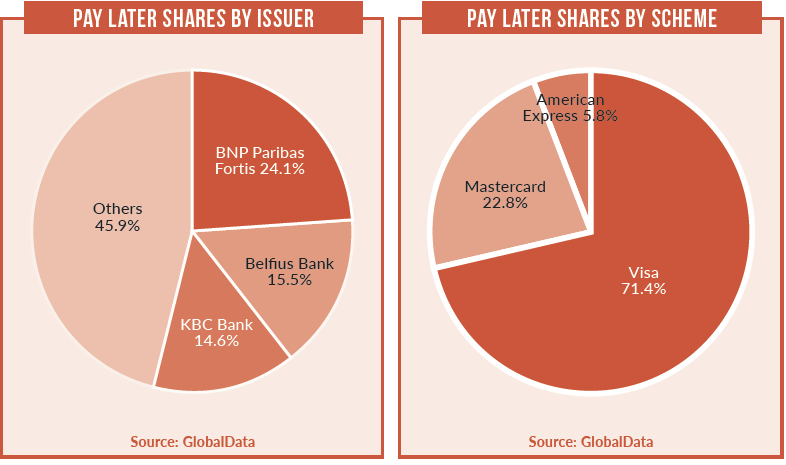

Pay-later cards

Pay-later cards are not very popular in Belgium, primarily due to consumer preference for debt-free payments. The ready availability of overdraft facilities also tempers demand.

Pay-later cards represented only 12.5% and 15.5% of overall payment card transaction volume and value respectively in 2018, but with the debit card market inching towards saturation, the underserved pay-later space could prove lucrative for banks, which are providing pay-later cards as part of bundled packages, and offering co-branded cards.

E-Commerce

The e-commerce market grew significantly from $7.30bn in 2014 to $13.18bn in 2018 at a CAGR of 15.9%.

Improvements in technology and rising online and mobile penetration have enhanced consumer confidence in online transactions. To capitalise on this, online retailers have introduced events such as Singles Day and Belgian Friday.

With the introduction of alternative payment solutions such as Google Pay and PayPal, the market is anticipated to grow further.

Prepaid growth

The prepaid card market registered a significant decline between 2014 and 2018 in terms of cards in circulation, largely due to the retirement of Proton cards in December 2014.

Proton cards were the most widely used prepaid card for low-value transactions, but with an increasing number of consumers using Bancomat cards, the Proton was phased out. However, banks are promoting prepaid card uptake by offering them as part of bundled account packages.

BNP Paribas Fortis, for example, offers customers a prepaid card with a Hello4You account. Comfort Pack account holders can opt for a credit card or prepaid card, while Premium Pack account holders can opt for both card types.

POS Growth

The number of ATMs fell marginally between 2014 and 2018, at a CAGR of -0.8%. A CAGR of -1.2% will be recorded over the next five years, with the number of ATMs falling to 7,781 by 2022 as banks close ATMs and branches.

Overall, the number of bank branches fell from 7,085 in 2014 to 6,150 in 2018. ATM use has also declined as consumers move to online and mobile banking. The number of POS terminals recorded a CAGR of 0.7%, increasing from 183,208 in 2014 to 188,032 in 2018, with the figure set to reach 206,921 by 2022.

Companies now offer integrated POS solutions. In 2017, myPOS launched an omni-channel payment package for SMEs in Belgium, enabling them to accept all major card schemes, and Ingenico and telecoms operator Orange Belgium launched the Orange Pro Payment mPOS solution for SMEs.