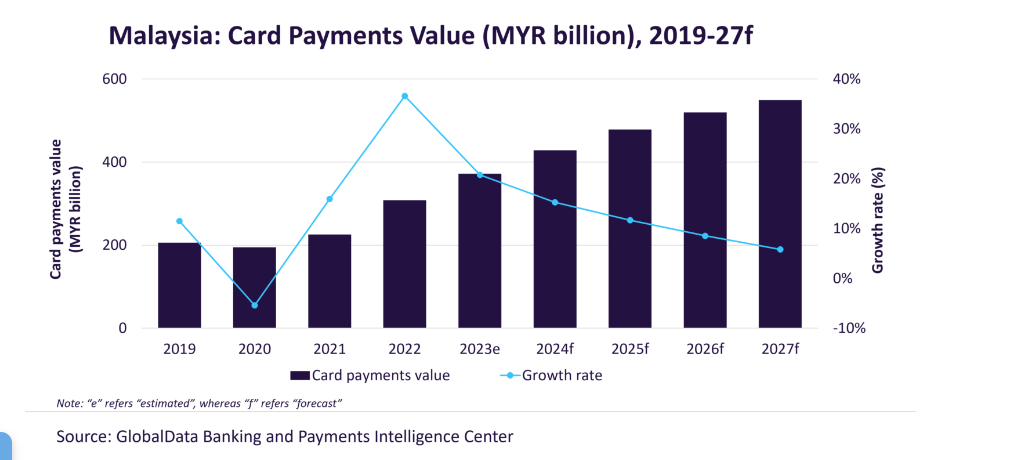

Malaysia’s card payments market is estimated to grow by 20.8% to reach MYR371.8bn ($84.5bn) in 2023, driven by a significant shift in consumer preferences towards non-cash payment methods and recovery in consumer spending, according to GlobalData, publishers of EPI.

GlobalData’s Payment Cards Analytics reveals that card payments value in Malaysia declined by 5.4% in 2020 as its economy fell into recession and both consumers and businesses cut down on spending.

Card sector growth of 36.6% in 2022

However, with the economy reviving from the Covid-19 pandemic, the country’s card market registered a healthy growth of 15.9% in 2021, followed by a higher growth of 36.6% in 2022.

Kartik Challa, Senior Analyst Banking and Payments at GlobalData, said: “Malaysia has traditionally been a cash driven society with cash accounting for 58% of the total payment volume in 2023. However, its share within the overall payments is on decline owing to the rising consumer preference for electronic payments. On the other hand, card payments have been on the rise supported by the concerted efforts by the government coupled with improvement in payment infrastructure.”

The Malaysian government has also been taking several steps to push cashless payments in the country. One of the initiatives was to make it mandatory for all government agencies to offer electronic payment options to citizens for payment of government services from March 2022. This allows citizens to pay for government services such as utility bill, fees and taxes using various digital payment modes such as debit and credit cards at government portals, as well as by internet banking, at ATM and kiosks.

Cap on interchange fees boosts card usage

Another initiative was the introduction of cap on interchange fees, with an aim to encourage merchants to accept card payments. Effective from 1 January 2023, interchange fee was capped at 0.10% on domestic debit card scheme, from 0.15% previously. Similarly, interchange fee on credit cards was reduced from 1.10% to 0.60%. However, this fee remained unchanged for international debit cards at 0.27%.

In terms of consumer preference, credit and charge cards are widely preferred when it comes to usage, with credit and charge cards accounting for 59.2% of the total card payments value in 2023. The increase in consumer demand for credit, especially from the growing middle-class, has helped the growth of credit and charge card transactions. Benefits such as discounts, cashback, reward points, and instalment facility have also driven the credit and charge card use.

Debit cards, on the other hand, account for the remaining 40.8% share. Although debit cards are traditionally preferred for cash withdrawals, they are now increasingly being used for payments as well – especially low-to-medium value transactions. This has been driven by rising consumer awareness, banks offering contactless debit cards, and the expansion of the country’s POS network.

Challa added: “Government initiatives to push electronic payments, economic recovery and opening of businesses have all benefitted payment card market. Although growing inflation and rising interest rates pose some challenge in short run, these are unlikely to disrupt the overall growth trajectory as Malaysia’s card payments market, which is set to grow at a compound annual growth rate (CAGR) of 10.3% between 2023 and 2027 to reach MYR549.5bn ($124.8bn) in 2027.”