Plutus aims to bring blockchain to the masses, creating a lifestyle around the cryptocurrency opportunity. Briony Richter speaks to CEO Danial Daychopan and marketing head Peter Panayi about what the business can deliver

Although there has been a global craze surrounding cryptocurrencies, especially Bitcoin, it is the technology behind it that can open the door to more accessible solutions.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Originally created for payments and settlement transactions, blockchain has the potential to change how consumers access data worldwide. Plutus, a mobile application for making contactless cryptocurrency payments, aims to change the way people view cryptocurrencies and bring them safely into their daily lives, accelerating mass adoption.

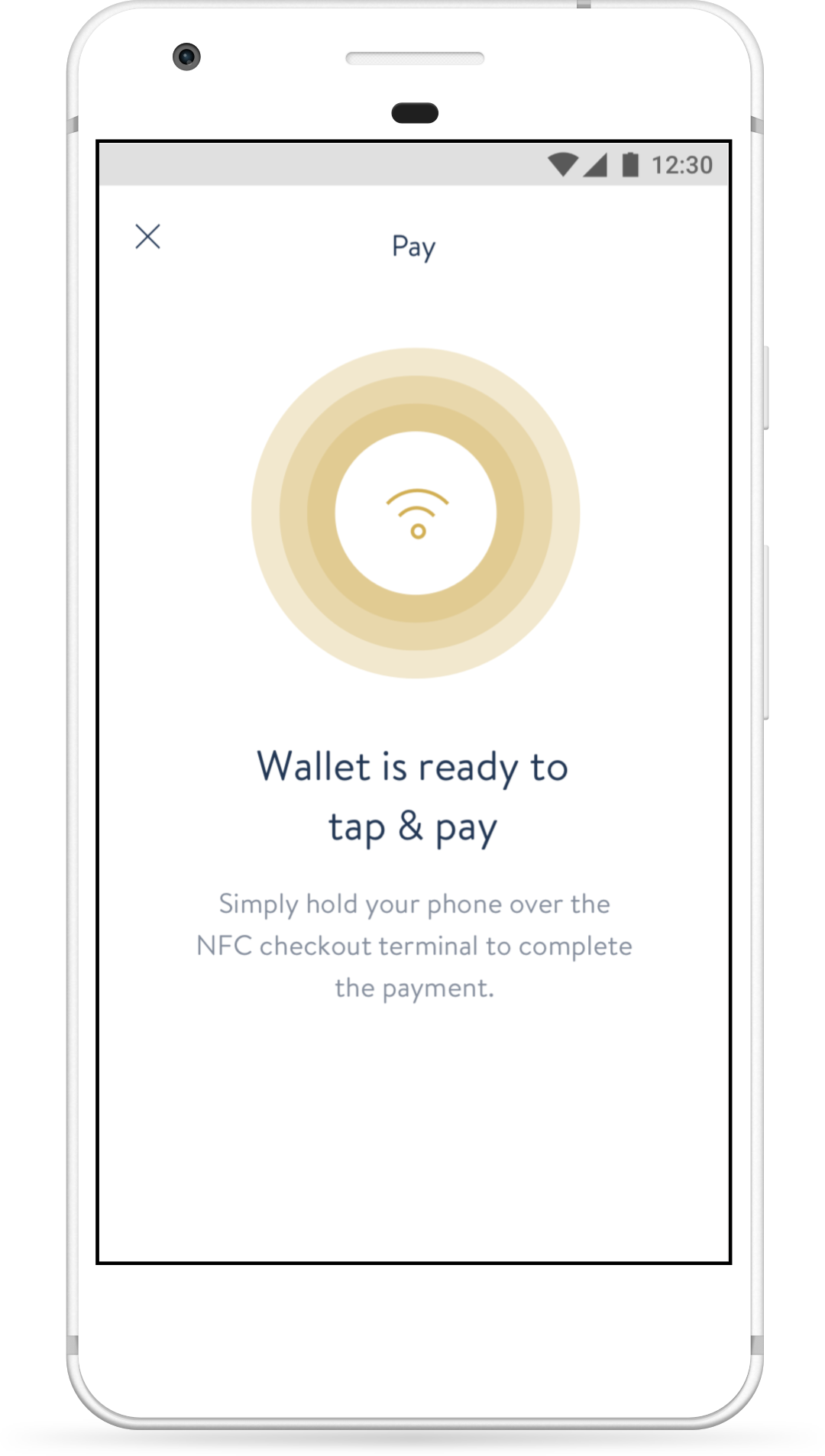

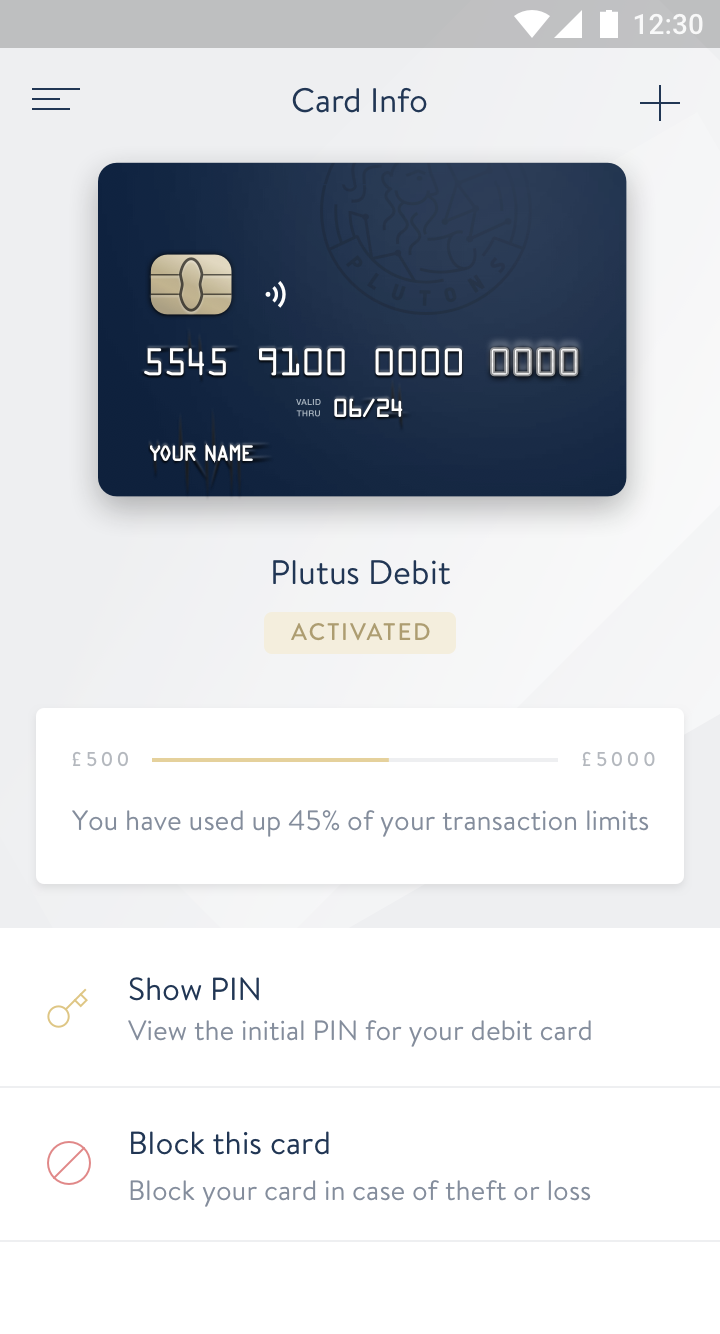

Plutus has two core products: Plutus Tap & Pay is a mobile app that allows iOS and Android users to make payments using Bitcoin and Ethereum at any contactless-enabled debit card terminal. The product is accepted by all merchants that Visa or Mastercard. In addition, Plutus offers rewards for every deposit made; they are paid to customers in Plutons, which can be used to make more purchases without fees.

The other product is PlutusDEX, is an exchange that provides liquidity for the Tap & Pay app. As well as the three cryptocurrencies, sterling and euros are also present, with the company looking to add US dollars soon.

With numerous cryptocurrency and blockchain companies in the market, Plutus CEO Danial Daychopan tells EPI what sets his business apart from the rest: “The PlutusDEX integrates an Ethereum smart contract, which offers unparalleled transparency and decentralisation when bridging the money we know with the nascent, growing world of cryptocurrencies.

“As Plutus never stores any user deposits, this means there is no central point of failure.”

Describing the methodology further, Daychopan adds: “By the time a user transfers digital currencies to Plutus, escrowed funds are already in place by users on the PlutusDEX. These funds are then only released if the transfer has been explicitly verified on the Bitcoin or Ethereum blockchain with a solid number of confirmations.

“From a security perspective, this is a state of-the-art method for avoiding intermediate counterparties and centralised storage of value which is only possible due to the immutable nature of blockchains with a strong enough hash rate, network distribution, and hashing algorithm. Plutus doesn’t verify the transactions; Bitcoin and Ethereum do.

“Notably, a normal centralised system is forced both store or manage user funds, as well as ensure payment confirmations and maintain solvency for cryptocurrency balances. In Plutus, these aspects are circumvented by design, because users transact with other users and the verification occurs on an external blockchain.

In this way, card balances are managed by the card issuer and all payments verification is handled by a cloud of Bitcoin and Ethereum miners. In this manner, the avoidance of a centralised point of failure alone already conveys a significant security advantage over competing platforms.”

Pluton

Pluton is the in-app cryptocurrency and acts as a loyalty rewards token.

Head of marketing Peter Panayi explains: “Pluton is a utility token, similar to air miles and rewards users for transactions made on the blockchain. We allow for streamlined transactions that are securely processed using next-gen technology, converting crypto into fiat currency seamlessly. We are essentially a technology service company with a focus on creating as little friction to the customer as possible to give them the confidence to use crypto in an everyday use case.

Panayi adds: “No one is doing this right – we are unique in our clear and transparent approach, giving customers the best service and care. Taking care of our community is fundamental. It’s been an exciting journey so far, and we believe that our solid approach to the regulatory aspect of KYC and AML sets us apart from our peers. We take these matters seriously; especially being a pioneer in the space, one needs to keep their eye on regulatory matters.”

There are fundamental challenges with blockchain, and organisations need robust KYC processes to tackle money laundering and fraud; however, its future is bright. For banks and financial institutions, payment settlements can be significantly improved by blockchain technology.

With legacy systems pulling down banks’ functionality, blockchain could eliminate some processes and positively disrupt the way we pay and trade. Despite its volatility, Bitcoin has proved how blockchain can provide a more seamless way to store data and value.

In December 2017, Swiss bank UBS announced it would be leading a pilot to harness Ethereum smart contracts to improve data quality ahead of MiFID II. Barclays, Credit Suisse, KBC, SIX and Thomson Reuters all joined the venture, which sets out the benefits of blockchain in a broader context than just settlement and clearing. Creating a platform that can allow people to bring cryptocurrencies into their day-to-day lives is what Plutus aims to do. The end goal is to enable consumers to pay with cryptocurrencies anytime and anywhere.