Use of cash for consumer payments remains high in Nigeria, especially among the rural population. This is primarily a result of low public awareness of other instruments, and limited access to banking infrastructure.

However, the Central Bank of Nigeria (CBN) has taken steps to improve this situation, the latest of which is the introduction of rules to establish Payment Service Banks. As part of its Financial System Strategy 2020, the CBN is focusing on bringing unbanked consumers into the banking system, and promoting electronic payments in the country.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Banks are also attempting to address the issue by launching basic, low-cost bank accounts, expanding the payment infrastructure, and looking to change Nigerian consumer payment habits.

A rise in the economically active population, the advent of digital-only banks, the growing popularity of online shopping, the gradual acceptance of cards among retailers, and the proliferation of new payment solutions will help drive electronic payments in Nigeria.

To augment the CBN’s financial inclusion programme, commercial banks in Nigeria are striving to enable unbanked individuals to access formal financial services by expanding the banking agent network in new regions, as well as launching self-service terminals.

Mobile money operators and telecom companies are also participating in the financial inclusion programme. Airtel Nigeria, for example, is considering launching a payment service bank. In 2016, United Bank for Africa, in collaboration with Visa, launched the SmartMoney banking service, which comprises a prepaid card and a mobile app, enabling users to make in-store purchases and withdraw cash from ATMs.

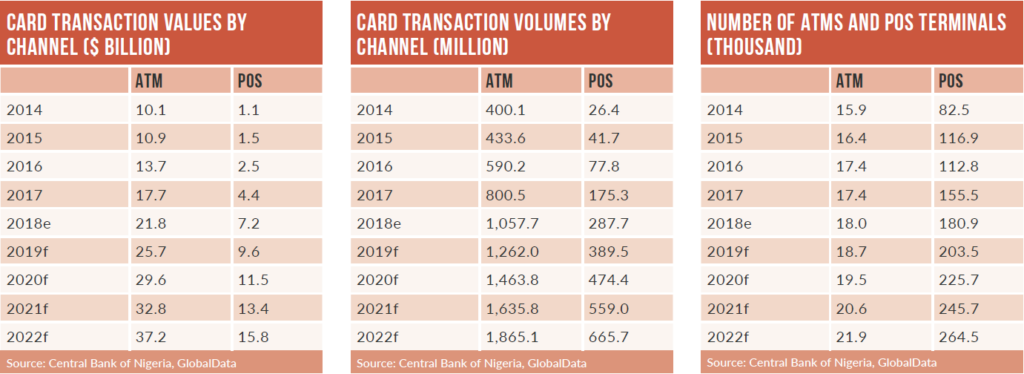

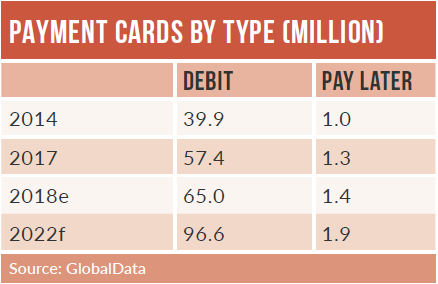

Pay-later cards are not popular in Nigeria, with a penetration of 0.7 cards per 100 individuals – the lowest among peers such as South Africa and Egypt. The adoption and use of credit cards has be partially hindered by economic uncertainty, with banks becoming wary of unsecured consumer lending.

The pay-later card market is, however, expected to register robust growth in terms of transaction value and volume between now and 2022, supported by growing demand for consumer credit – especially among the increasing middle-class and high-income populations.

The Nigerian e-commerce market recorded a robust CAGR of 29.8%, rising from NGN163.1bn ($448.56m) in 2014 to $1.27bn in 2018. Banks and investment companies are launching their own e-commerce platforms to benefit from this.

While traditional payment instruments – including cash, cheques, bank transfers and payment cards – remain the preferred method of payment for online shoppers, alternative payments such as KongaPay, Paga and PocketMoni are also used.