Israel is one of the most developed payment card markets in the Middle East. Despite this and numerous central bank efforts, however, consumers remain largely inclined towards cash, with debit cards in particular struggling for acceptance

Consumers in Israel are prolific users of payment cards.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The country registered the highest frequency of payment card use in comparison to its peers in 2016, with 155.4 transactions per card, as compared to Saudi Arabia with 99.0, Iran with 62.0, Kuwait with 54.9, the UAE with 49.8, Lebanon with 31.3, Oman with 22.4 and Bahrain with 18.1.

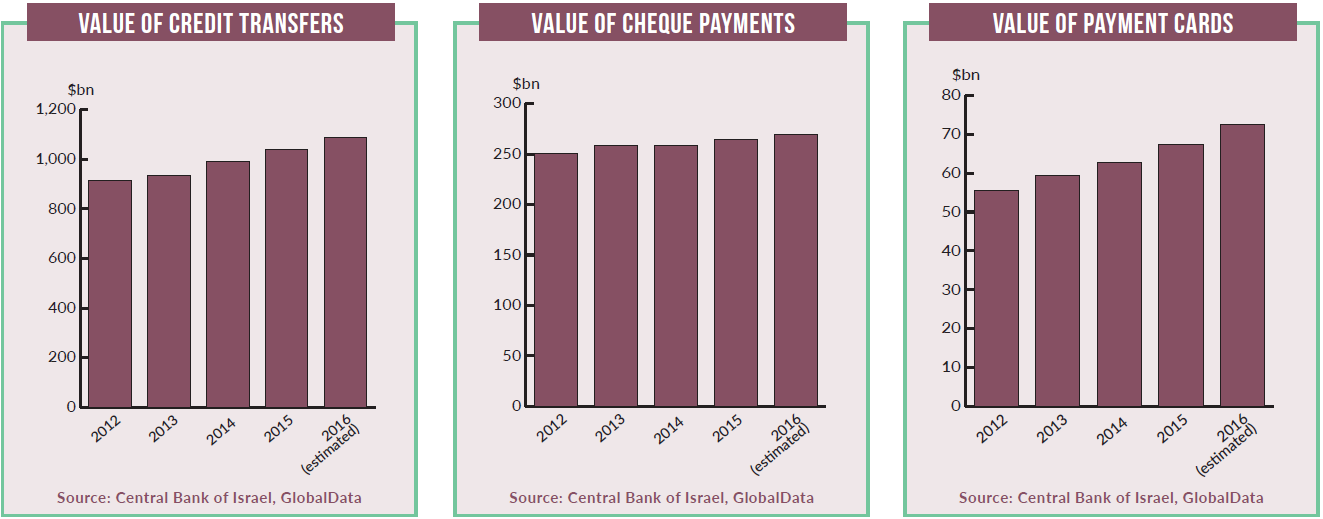

Despite growth in non-cash payments in the last decade, Israeli consumers are still strongly inclined towards cash. The Bank of Israel has made several regulatory interventions to boost electronic payments and reduce dependence on cash, such as introducing a cap on cash transactions.

Israeli regulators are looking to open up competition by allowing new types of banking, such as mobile-only banks.

In February 2017, Bank Leumi launched Pepper, a mobile-only banking service offering savings and lending products. In January 2015, Bank Leumi launched a service enabling personal customers from all banks to open an account via the internet or mobile apps, without needing to visit a branch.

Debit cards

Debit cards

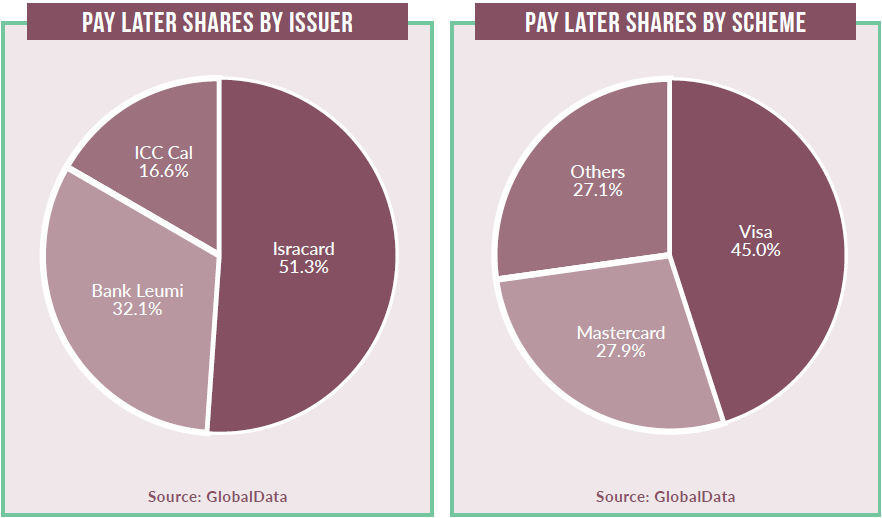

Israel’s payment cards market is dominated by pay later cards, with limited adoption of debit cards.

All credit cards are a combination of deferred debit and credit cards, and function more like charge cards. Generally, credit cardholders are billed for purchases at the end of a month; however, in Israel the total outstanding amount in a given month is automatically debited from the customer’s current account.

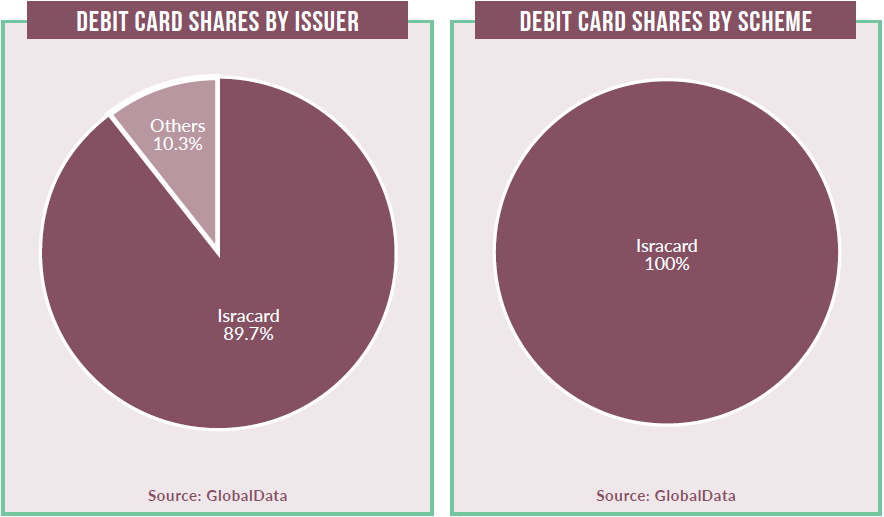

Adoption of debit cards remained low as retailers were reluctant to accept them due to the lengthy transaction process and high merchant service charges. While debit cardholders were charged immediately, amounts were credited to retailers’ accounts at a later date – similar to the timing of deferred debit transactions – typically after a month.

In addition, retailers paid high merchant service charges for debit card transactions, at a similar rate to credit card transactions. With no incentive to favour a debit transaction over a credit transaction, merchants had little incentive to accept debit cards.

Debit card penetration in Israel was 10.3 cards per 100 individuals in 2016, lower than peers Iran (337.3), the UAE (109.3), Bahrain (97.4), Kuwait (93.1), Oman (85.8), Saudi Arabia (75.8) and Lebanon (33.4).

The central government took several initiatives between 2012 and 2016 to curtail cash transactions and encourage debit card use, including requiring banks to issue debit cards free of charge to new and existing accounts, reducing interchange fees on debit card transactions, and abolishing bank fees for debit card transactions. These initiatives are expected to increase overall debit card penetration and use.

Banking sector

Banking sector

A key aspect of Israel’s payment cards market is the entrenched positions held by the three main credit card issuers, owned by the country’s main banking groups.

The dominance of Isracard, Leumi Card and ICC Cal has long gone unchallenged for several reasons, including the barriers to entry for foreign issuers which lack the wide branch networks and distribution points of domestic issuers.

Another factor is that Israel is, at least in card payment terms, a small country. This has not gone unnoticed by banking regulators, which are cracking down on the perceived duopoly of Bank Hapoalim and Leumi Card. As a result, both banks have been asked to separate ownership of their credit card companies.

The country‘s third main credit card issuer, ICC Cal will be unaffected for four years, when the issue will be re-examined. Standalone credit card units are encouraged to become banks and will be subject to various incentives such as lower capital requirements.

Alternatives

Alternatives

A growing preference for secure electronic payments and deeper smartphone penetration saw credit card companies, payment service providers and telecoms companies launch alternative payment solutions, the latest being Mastercard’s Masterpass in November 2015.

Users can shop online without providing payment and shipping information on every purchase. For online payments, Masterpass allows users to pay from a list of pre-stored cards and shipping information stored in a digital wallet.

The fast-growing e-commerce market is also supporting growth in alternative payments in Israel. PayPal, ICC Cal and mobile carrier service provider, Pelephone have active presences in the country.