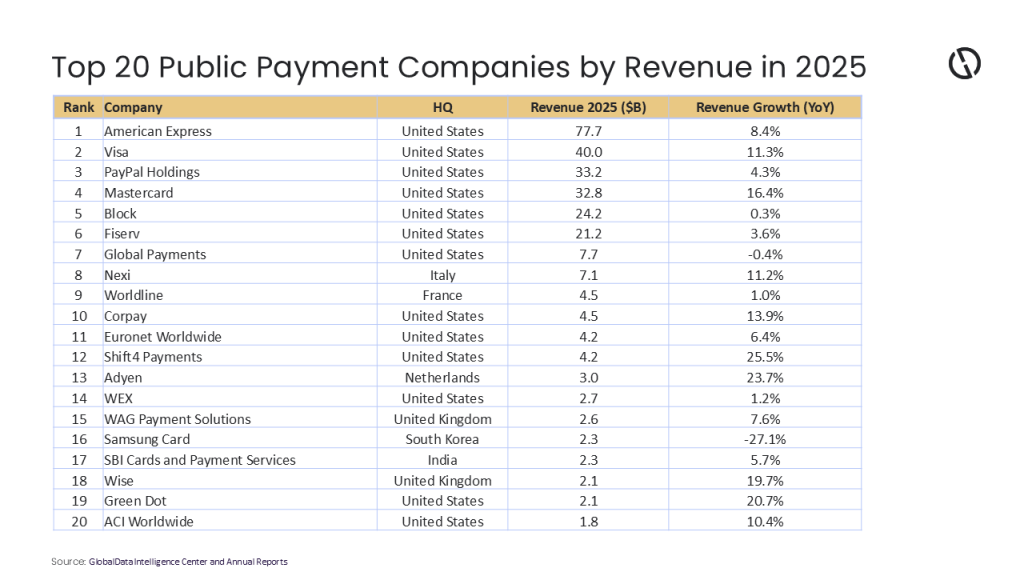

The global payments industry delivered another year of expansion in 2025, with network operators benefiting from international commerce and payment volume growth even as transaction processors faced slower merchant spending and intensifying competition. The world’s 20 largest listed payment companies generated a combined revenue base of $280bn in 2025, with growth increasingly concentrated among firms exposed to cross-border transactions, digital commerce, and software-integrated payments, according to GlobalData, publishers of EPI.

Murthy Grandhi, Company Profiles Analyst at GlobalData, said: “American Express (AmEx) sits atop the leaderboard with an 8.4% rise in revenue to $77.7b. Visa ($40bn, +11.3%) and Mastercard ($32.8bn, +16.4%) are growing faster than AmEx despite processing trillions in transactions through their network rails. Mastercard’s growth reflects a deliberate pivot into value-added services: data analytics, cybersecurity solutions, and open banking APIs that now account for a growing share of revenue. The card business is mature; the data business is not.”

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

PayPal underperforms

PayPal’s 4.3% growth, meanwhile, is the most consequential underperformance in the sector. The company processes over $1.5tn in payment volume annually, yet revenue barely tracks inflation. The problem is structural: PayPal remains heavily exposed to e-commerce checkout, a market where competition from Apple Pay, Shop Pay, and card-linked offers has intensified. Management’s pivot toward advertising and BNPL (buy now, pay later) integrations has yet to move the needle materially.

Mid-tier challengers outperform market

The real story, however, lies among the mid-tier challengers. Shift4 Payments (+25.5%) and Adyen (+23.7%) are growing at a rate that dwarfs every company above them in the revenue rankings. Shift4’s expansion is driven by its aggressive move into hospitality, stadiums, and gaming verticals — industries that were historically underserved by payment infrastructure and are now rapidly upgrading their point-of-sale technology. Adyen’s growth reflects something more structural: enterprise merchants increasingly want a single global payments platform, not a patchwork of acquirers and processors. Adyen has positioned itself as precisely that — and it is winning contracts accordingly.

Green Dot, Wise cash in on democratisation

Grandhi added: “Wise (+19.7%) and Green Dot (+20.7%) represent a different but equally significant trend: the democratisation of financial services. Wise’s cross-border transfer infrastructure continues to take share from correspondent banking networks, particularly on corridors like the UK-India and EU-Southeast Asia. Green Dot’s surge reflects growing demand for prepaid and banking-as-a-service products among America’s underbanked population — a segment that has historically been ignored by traditional banking infrastructure.”

Merchant acquirers and payment processors delivered mixed results. Fiserv grew 3.6%, while Global Payments recorded a slight revenue decline. These firms face increasing pricing pressure as merchants gain access to more payment providers and integrated software platforms.

The weakest performer was Samsung Card, whose revenue declined 27.1%. The sharp contraction likely reflects a combination of weaker consumer credit demand, regulatory pressures, and normalisation following prior-period strength. By contrast, SBI Cards and Payment Services benefited from India’s expanding middle class and ongoing shift toward formal digital payments.

Sector outlook

GlobalData anticipates that the industry’s outlook remains favourable, supported by continued digitisation, rising e-commerce penetration, real-time payments, and increasing adoption of embedded finance. However, growth is likely to become more uneven. Persistent inflation, higher-for-longer interest rates, slowing global trade, US-China tensions, conflicts in Eastern Europe and the Middle East, and increasing regulatory scrutiny of payment fees could weigh on transaction volumes and cross-border activity.

At the same time, payment companies that enable international commerce, software-driven merchant solutions and business-to-business transactions appear best positioned to outperform.

Grandhi concluded: “The next phase of competition will likely be defined less by who processes the most payments and more by who owns the customer relationship, data layer, and software ecosystem surrounding those payments. In that race, the industry’s fastest-growing challengers are beginning to narrow the gap with its established giants.”