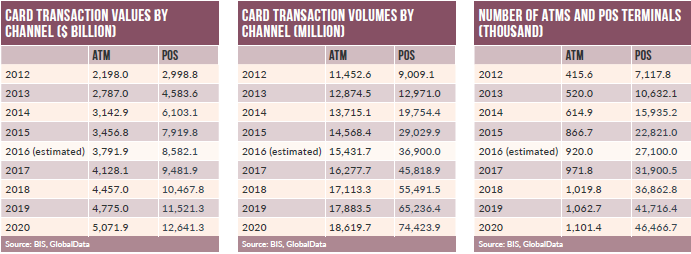

China is Asia’s largest payment cards market in terms of card transaction value and volume, accounting for 77.1% and 45.8% shares respectively in 2016. GlobalData looks at the regional giant

China’s average annual spend per card is high, at $1,388.7, as compared to peers such as Malaysia ($695.2), Thailand ($492.8), the Philippines ($351.7), Indonesia ($283.5) and Cambodia ($112.6).

Go deeper with GlobalData

Cash, however, remains a popular payment instrument among Chinese consumers, especially in rural areas. This is primarily a result of limited knowledge of the benefits of electronic payments, and limited access to banking infrastructure.

The government and banks have begun to provide basic financial access to the unbanked population by expanding banking infrastructure, launching new branches and making efforts to change consumer payment habits.

As a result, payment cards are gradually becoming more accepted, with their use growing during 2012–2016. The share of the Chinese population aged 15 or above with a bank account rose from 69.3% in 2012 to 84.6% in 2016.

How well do you really know your competitors?

Access the most comprehensive Company Profiles on the market, powered by GlobalData. Save hours of research. Gain competitive edge.

Thank you!

Your download email will arrive shortly

Not ready to buy yet? Download a free sample

We are confident about the unique quality of our Company Profiles. However, we want you to make the most beneficial decision for your business, so we offer a free sample that you can download by submitting the below form

By GlobalDataA rise in the economically active population and per capita disposable income, the growing popularity of online shopping, the increased acceptance of cards at retailers and the adoption of contactless technology supported growth in payment cards, and the emergence of digital-only banks is likely to accelerate a shift towards electronic payments.

WeBank launched in January 2015 to become China’s first digital-only bank, allowing consumers to conduct transactions entirely online and via mobile phones. It was followed by the launches of MYBank and Baixin Bank in June and November 2015 respectively.

China UnionPay (CUP) is the sole scheme provider of payment cards. According to central bank regulations, all banks and card issuers operating in the country are required to route renminbi-based transactions through CUP’s electronic payment network.

However, following a complaint by the US via the World Trade Organisation about discrimination against foreign companies in 2012, the WTO directed the Chinese government to open up its payment cards market to foreign operators.

In October 2014, the Chinese government announced its decision to allow foreign companies to set up their own payment card clearing businesses, with effect from 1 June 2015. In June 2016, however, the central bank set new rules enabling foreign competitors to begin operations in the market.

This move by the Chinese government is anticipated to intensify competition in the payment cards market, and reduce CUP’s dominance. However, Visa and Mastercard have far to go before they can gain substantial market share from CUP, as they need to build infrastructure from scratch.

Contactless mobile payments and consumer preference for secure and convenient payment services are growing with the launches of Apple Pay, Samsung Pay, Huawei Pay and Mi Pay in 2016, in association with CUP.