Indian mobile banking usage has continued to grow, demonstrating the extent to which India’s demonetisation efforts are shifting consumer banking habits

In November 2016, the Indian Government issued out an unprecedented policy move. The two highest denomination banknotes, the INR500 and INR1,000 bills, were demonetised, rendering just about 86% of the country’s currency invalid in under 24 hours.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The reason for this was to get rid of illegal financial activity and fraud. Since then the Indian mobile banking sector has erupted. The Indian government is developing programmes to better serve the unbanked and is insisting that banks do the same.

Alternative payments in the Indian mobile banking space

The Indian government had started paving the way for more mobile banking inclusion back in 2013. The Reserve Bank of India (RBI) set up a special committee to explore the possibilities of introducing an SMS-based payment system. This would enable millions of Indian people that were currently unbanked to conduct banking transfers via their mobile phones.

Now there are numerous alternative solutions and providers pushing to expand Indian mobile banking capabilities.

Axis Bank

Axis Bank launched a mobile payments service that enabled users to send money to each other through WhatsApp, Facebook, Twitter, email, and phone contact lists. Pushing past the traditional mobile banking transfer, Axis Bank tapped into the social media space. Extremely popular among millennials, many banks and financial organisations are exploring and testing the benefits of payments through the sites that people visit most.

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalDataDeveloped with Singapore-based social payments vendor Fastacash, the Ping Pay app enables P2P fund transfers and mobile top-up through NPCI’s Immediate Payment Service. Axis Bank customers can download the app and sign up for the service using their registered mobile number. Then they are able to link their online banking payment cards.

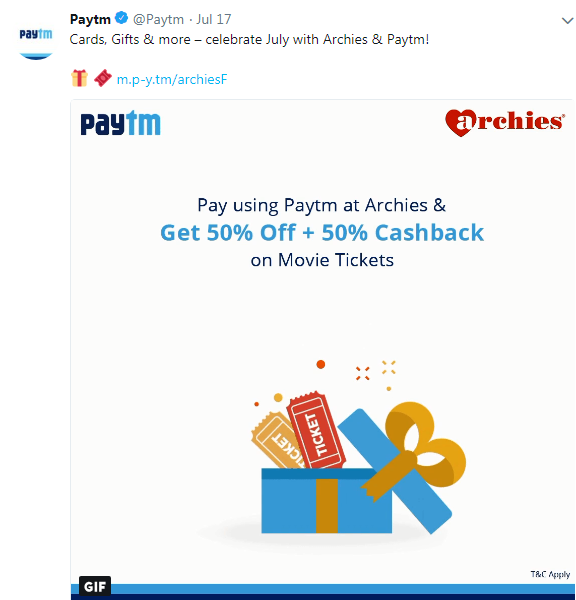

Paytm

Paytm was founded by Vijay Shekhar Sharma and is the leading online payment portal in India. It’s popular for its ease of use and a wide range of promotional offers. Merchants can sign up to use Paytm without even having a bank account. The Paytm wallet can receive money and users can spend from their wallets at retailers that accept Paytm.

Along with mobile data deals and cashback on electricity, Paytm also offers a range of different recreational promotions. These include cashback on flight bookings, free movie tickets and offers at various restaurants and shops.

In 2017, the payments company registered 200 million users. Sharma now looks to 2020 with the goal of reaching 500 million users.

Samsung Pay

Samsung Pay launched in India in March 2017, enabling consumers to pay using contactless technology on Android phones.

Supporting banks and card issuers include Axis Bank, Citibank, HDFC Bank, ICICI Bank, SBI, Standard Chartered Bank, and American Express. There are also a number of supporting merchants, including Lifestyle, Max, Café Coffee Day, Pizza Hut, Big C, Croma, Reliance Digital, Apollo Pharmacy, SPAR Hypermarket, and INOX.

Furthermore, Samsung Pay’s integration with Paytm has enabled Samsung Pay users to connect their mobile wallet to the Paytm service.

The Indian mobile banking ecosystem rapidly increased after demonetisation. A whole new and very large population started to adopt digital payments. The sector shows no signs of slowing down.