The rising cost of living and inflation have impacted UK consumers’ spending habits, and some consumers are reverting back to cash as it is easier for them to stay on top of their expenses. But this circumstantial revival in cash usage will not slow down the decline of cash in the UK economy.

Cash payments have been on a steady decline in recent years as alternative payment tools such as contactless cards and mobile wallets have merged. GlobalData’s Payment Instrument Analytics estimated that the value of cash payment transactions declined at a compound annual growth rate (CAGR) of 13.61% between 2012 and 2021. But over the same period, the value of card payment transactions increased at a 6.3% CAGR and mobile wallets increased at a 30.8% CAGR.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

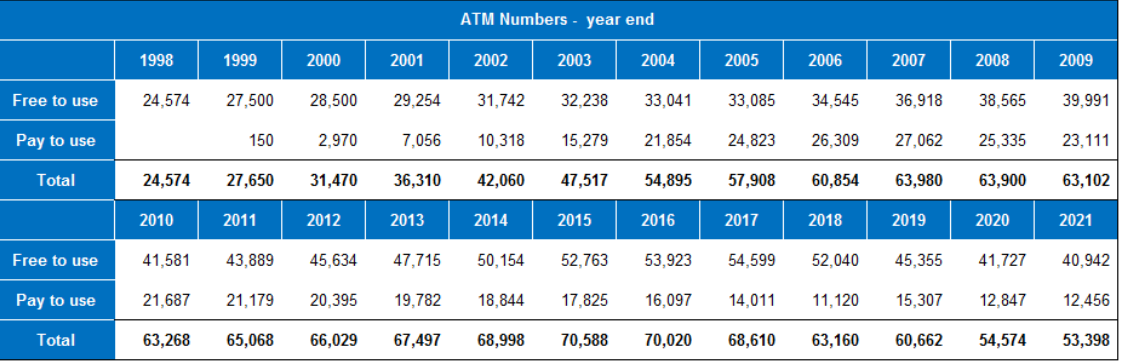

UK: ATM numbers peaked in 2015

In addition to competing with new payment tools, cash is also becoming difficult to access in some parts of the UK as bank branches and ATMs are closing down around the country. According to GlobalData’s Payment Cards Analytics, the number of ATMs in the UK decreased by 4,000 between 2020 and 2021, and it is forecasting an additional 8,300 ATMs to close by 2026. The closure of bank branches and ATMs is mainly due to a decline in the number of people using those services as they have adopted online banking. With fewer people using these services, the cost of operating branches is becoming too expensive for banks.

Though cash usage is predicted to continue declining according to GlobalData’s Payment Instrument Analytics, it will still remain within the UK’s payment infrastructure. As long as millions of people rely exclusively on cash, it will be necessary for the UK government to maintain access to it. But this will be a challenging endeavour due to the growing number of businesses that are no longer accepting cash. Some UK consumers may find themselves in the difficult situation of having cash but not being able to use it with some businesses.

The need for government intervention

Government intervention is necessary to protect UK consumers who rely on cash. The UK government should be more proactive in protecting cash usage, and it could look at how other countries such as Sweden are dealing with a similar decline of cash usage. According to GlobalData’s Payment Instrument Analytics, Sweden’s cash transaction value decreased by $7.8 billion between 2011 and 2021. To maintain access to cash, the Swedish government passed a bill in 2019 that requires banks to provide cash access and minimum cash services to Swedish consumers and businesses.

Cash is no longer king in the UK economy, and there is no legal obligation for businesses to accept it. The UK government needs to find a long-term solution to the cash issue, otherwise it is likely to have a cash-reliant population that is marginalised from the economy.