Crypto-backed lending is on the rise again, following the wider crypto market crash in 2022 which caused mass loan defaults and liquidation. By mid-2025, Coinbase alone hit $500m in on-chain loans originated; a 10-fold growth achieved within three months of Q2, pointing to newly-emerging opportunities and huge growth potential across the lending space. Nevertheless, South Korea’s Financial Services Commission halted all new crypto lending with immediate effect in August 2025 due to increasingly-overleveraged loans causing a $1bn liquidation event; highlighting the continued risks associated.

All types of credit products are moving on chain which traditional lenders cannot afford to ignore. In addition to direct personal lending, Coinbase integrated with the biggest US credit card lender JPMorgan to link spending and rewards between a credit card and crypto wallet.

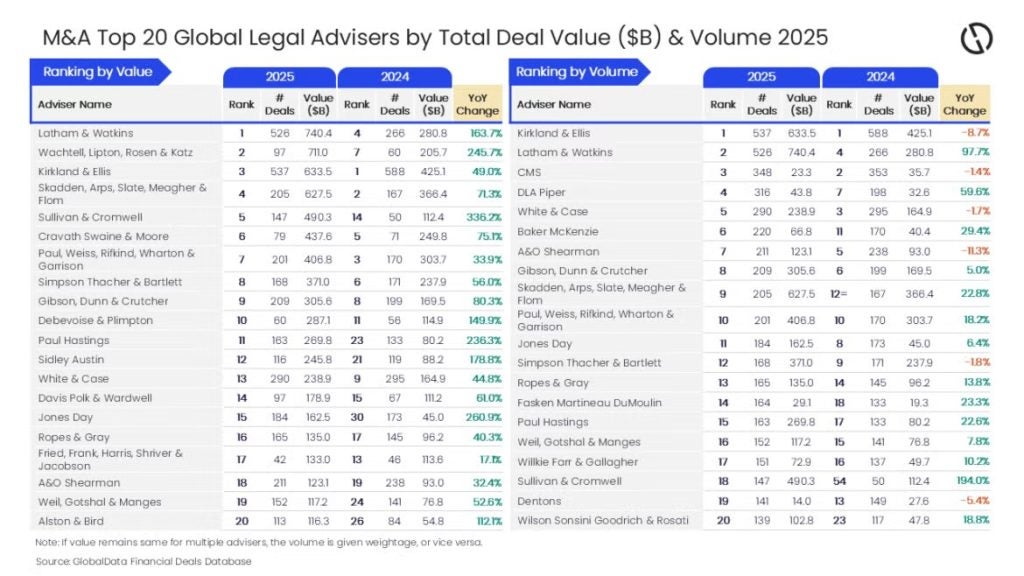

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

GlobalData Global Retail Banking Analytics

Customers will be able to fund their crypto wallet from their credit cards, redeem reward points to USDC, and link Chase accounts directly with Coinbase wallets. GlobalData’s Global Retail Banking Analytics shows JPMorgan holding 19.2% of the total US credit card debt outstanding worth $1.2tn, opening a huge potential for Coinbase’s popularity to become a preferred crypto wallet.

In addition, the first crypto-backed mortgage in Australia is now available on Block Earner’s waitlist following the company’s recent court victory against the Australian Securities and Investments Commission over licensing agreements. Bitcoin (BTC) holders will be able to access a home deposit up to Australian dollar A$5m ($3.2m) against their BTC without having to liquidate it. GlobalData’s upcoming report Targeting First-Time Buyers in Financial Services shows these advancements could redefine the struggling first-time buyer market, as 38% of new and prospective homebuyers own cryptocurrencies globally in 2025, compared to 23% of the average population. The US Federal Housing Finance Agency has also recently ordered Fannie Mae and Freddie Mac to consider potential borrowers’ crypto assets as collateral on single home mortgage loans.

Against this backdrop, South Korean regulators halted crypto lending activities in growing demand, until further regulatory clarity is achieved. Algorithmic lending on major exchanges, such as Upbit and Bithumb, allowed for overleveraged loans up to four times the value of the crypto asset collateral; resulting in 13% default and forced liquidation as BTC moved below $120k. With no intention of a complete ban, the Commission is working to clarify legal guidelines and improve investor safeguards with the ultimate goal of integrating South Korea’s outsized personal lending market worth half a trillion dollars within a secure digital finance system. Beyond growing customer demand, national regulation remains the main determinant force shaping the trajectory of emerging crypto opportunities globally.

Blandina Szalay is an Analyst, Banking & Payments, GlobalData

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalData